")

This article is for general informational purposes only. Mortgage rules, rates, and qualifying requirements vary by lender and mortgage type. This is not financial or mortgage advice. Confirm your specific renewal options, rate eligibility, and switching requirements with a licensed mortgage professional before making any decisions.

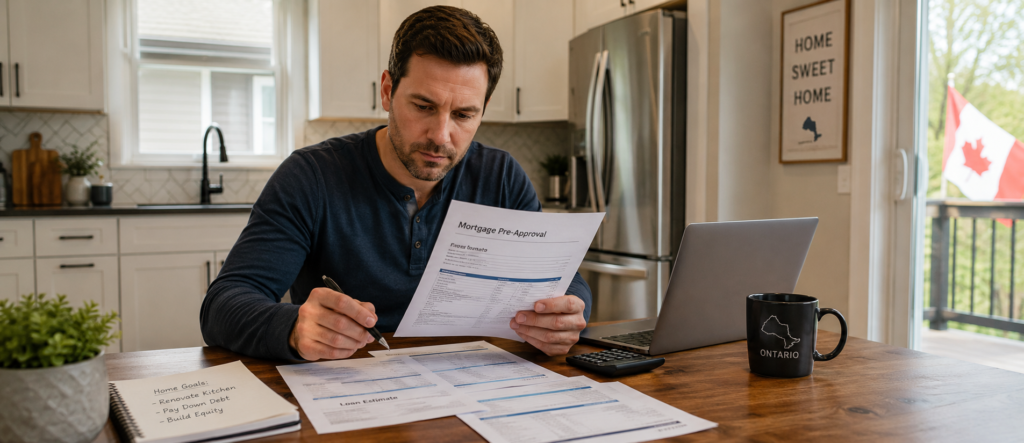

The renewal letter shows up a few months before your term ends. For most homeowners, it feels like a bill. You scan the new rate, sign the form, and send it back.

That is one way to handle it. But if you locked in during 2020 or 2021, the number in that letter is probably not the number you were used to. The monthly payment difference is real, and for a lot of careful homeowners in Brampton and Mississauga, that is the first number that gives them pause.

Before you sign, it is worth knowing what your actual options are. The letter from your lender is a starting point, not a final answer.

Who this is for: Brampton and Mississauga homeowners whose mortgage is renewing in the next 6 to 18 months, particularly those who locked in at low fixed rates during 2020 or 2021 and are approaching a new term in a different rate environment. Also for anyone wondering whether renewal is the right moment to consider selling.

Quick Answer

At renewal, you have three real options: negotiate with your current lender, who may not have opened with their best rate; explore switching to a different lender, where qualifying rules at renewal may differ from a new purchase (confirm current stress test requirements with your mortgage broker); or use renewal as a natural moment to decide whether selling makes more sense. Most homeowners only think about the first option. All three are worth knowing.

What a Mortgage Renewal Actually Is

When your mortgage term ends, the full balance does not come due. Your mortgage renews. You agree to a new rate and a new term for the remaining balance.

Most lenders send a renewal offer 90 to 120 days before the term ends. They will offer you a rate. They may not open with their best rate. The gap between what is in that letter and what is actually available, whether through negotiation or through shopping elsewhere, is often worth finding before you sign.

The balance at renewal is whatever principal remains. The amortization continues. The main thing that changes is the interest rate and the term you choose.

The Three Options Most Homeowners Do Not Know They Have

Option 1: Renew with your current lender

This is where most homeowners land by default. No new underwriting, no fresh credit check, no requalifying. It is the simplest path.

But simple and best are not the same thing. The rate for the homeowner who does not ask is usually higher than the rate for the homeowner who does.

A homeowner I work with was approaching renewal. Their bank had sent an offer. They were ready to sign. When they showed me the letter, I could see rates in the market were coming in lower. We went back to the bank together. It went back and forth. The bank came back with a rate much closer to what the market was offering.

That conversation is going to save them thousands of dollars over the course of the term. They told me they were glad they called before signing. That is the point. The renewal letter is not the final number.

Option 2: Switch to a different lender

Before you sign with your current lender, it is worth asking a mortgage broker what the current qualifying requirements are for switching lenders at renewal. The rules around straight switches at renewal changed in late 2024, and a straight switch, moving the same mortgage balance and amortization to a different lender, is treated differently from a refinance for qualifying purposes.

Many brokers confirm that straight switches may be handled differently from new purchases or refinances for stress test purposes. But the exact requirements depend on your mortgage type and lender. Ask your mortgage broker what applies to your specific situation before you start shopping around.

Straight switch vs. refinance: know which one you are doing

A straight switch moves the same loan balance and amortization to a new lender. A refinance changes the loan amount or the amortization period. These are handled differently for qualifying purposes, and the rules for straight switches at renewal changed in late 2024. Ask your mortgage broker what the current requirements are for your specific mortgage type and lender before comparing rates elsewhere.

Note: Credit unions are not all subject to federal guidelines and may follow different qualifying rules. Confirm with your mortgage broker.

Option 3: Sell

Renewal is one of the few moments where a homeowner looks at the whole picture at once: the rate, the payment, the equity, and where the household is heading. Most of the time those questions sit separately. At renewal they come together.

For Brampton and Mississauga homeowners who bought during 2018 to 2021, the equity position is often larger than people assume, even after the 2022 to 2023 correction. Some of the homeowners I work with realize at renewal that they are not actually locked into something that no longer fits. The home has done its job. The equity is real. The question is whether to stay on course or use this moment to redirect.

That is not the same as being in trouble. It is being in a position of choice.

I saw this play out with a seller I recently worked with. Their mortgage was coming up for renewal. Instead of signing a new term, they decided this was the right time to list. The market is slower than it was two years ago, but the property is selling. Renewal was not the problem. It was the moment the bigger question could not be ignored anymore.

If the equity is meaningful and the carrying costs no longer fit the direction the household is heading, renewal is the last natural pause before another multi-year commitment. If you are a Mississauga seller weighing your equity against your next move, the net proceeds picture matters as much as the listing price. For context on what sellers typically walk away with after costs, see How Much Will I Net After Selling My Home in Mississauga.

The Rate Reality for 2020 and 2021 Borrowers

Many homeowners who locked in five-year mortgages in 2020 and 2021 secured rates that have not been seen since. Renewal means choosing a new rate in a different environment.

The gap between those rates and what is available today is real. On a typical Brampton or Mississauga mortgage balance, the difference in the monthly payment is not a small adjustment. It is worth calculating the actual number before you make any decision, because the number you get from your broker may be different from the number that first lands in your inbox.

The Bank of Canada held its overnight rate at 2.25% at its most recent announcement in April 2026. That is well below the 2023 peak, but fixed mortgage rates follow bond markets rather than the overnight rate directly. What you will pay at renewal depends on the term and type you choose.

What matters most is the monthly payment you will actually live with, and whether the options available to you through negotiation, switching, or selling change that number in a meaningful way.

What to Check in the 90 Days Before Your Renewal

The mistake most homeowners make is not acting too early. It is waiting too long. By the time the renewal date is two weeks away, the window to compare and negotiate has mostly closed. Here is what to look at now.

| Check this | What it means for you |

|---|---|

| Your current balance | Your starting point for any comparison or negotiation. |

| The term you want | Shorter terms give flexibility if rates shift. Longer terms give predictability. Ask your broker which makes more sense given the current environment. |

| Fixed vs. variable | Variable rates follow the prime rate and the Bank of Canada’s overnight rate decisions. Fixed rates follow bond markets. The Bank of Canada held at 2.25% in April 2026 but flagged uncertainty around energy prices and global conditions. The right choice depends on your payment comfort and risk tolerance, not what worked in 2021. See: Fixed vs. Variable Mortgage in Ontario: How to Choose in 2026. |

| Refinance or straight switch? | A straight switch moves the same balance and amortization to a new lender. A refinance changes the loan amount or the amortization. These are treated differently for qualifying purposes, and the rules for straight switches at renewal changed in late 2024. Confirm with your mortgage broker what applies to your specific situation before shopping around. |

| Whether to sell instead | Worth asking plainly before you commit to another term. If the equity is meaningful and the carrying costs no longer fit the plan, renewal is the last natural pause before another multi-year commitment. |

Start the Conversation 90 to 120 Days Out

Most lenders will let you lock in a renewal rate up to 120 days before your term ends. That is your window. Use it.

Start 90 to 120 days out. Talk to a mortgage broker. Find out what your current lender is offering and what is available elsewhere. Then bring that comparison back to your current lender. As the homeowner in the story above found out, the bank’s first offer is almost never its final one.

The homeowner who starts early has options. The one who starts late has a deadline.

Ready to Sort Through Your Renewal Options?

If your mortgage is renewing in the next 6 to 12 months, that conversation is worth having before you sign.

Call Gaurang at 647-892-2411.

Key Takeaways

- Renewal is a decision point. The letter from your lender is an opening offer, not the final answer.

- The rate for the homeowner who does not ask is usually higher than the rate for the homeowner who does.

- The qualifying rules for straight switches at renewal changed in late 2024. Confirm with your mortgage broker what applies to your specific situation and mortgage type before shopping for a better rate.

- You have three real options: negotiate with your current lender, explore switching to a new one, or consider whether selling makes more sense.

- Start the process 90 to 120 days before renewal. Early gives you options. Late gives you pressure.

- For homeowners who bought in 2018 to 2021, the equity position at renewal is often more meaningful than they expect. That changes what is possible.

Bottom Line

The purchase price got you in. The renewal rate is what you live with for the next several years.

Sign when you understand what you are signing for.

Frequently Asked Questions

Does the mortgage stress test still apply at renewal?

The rules around the stress test for switching lenders at renewal changed in late 2024. A straight switch, moving the same mortgage balance and amortization to a new lender, is generally handled differently from a refinance or a new purchase for qualifying purposes. Whether the stress test applies to your specific switch depends on your mortgage type and lender. Confirm the current requirements with your mortgage broker before shopping for a better rate.

Can I negotiate my renewal rate?

Yes. The rate in the renewal letter is the bank’s opening position, not their only position. Many lenders will improve the offer when a borrower comes back with a competing rate or asks directly. Not every lender will move significantly, but the comparison is almost always worth making. Getting one outside quote before renewal is often the most effective thing you can do.

When should I start looking at renewal options?

90 to 120 days before your term ends. Most lenders allow you to lock in a rate up to 120 days out. Starting early gives you real leverage. Starting the week before gives you almost none.

What if I want to sell instead of renewing?

If your mortgage is renewing and selling is on your mind, that question is worth exploring before you sign a new term. You will want to understand your equity position, what a mortgage payout would cost if anything, and how the carrying costs compare to where you want to go next. Starting that conversation at renewal rather than after signing gives you much more room to move.

What is a straight switch?

A straight switch is moving your existing mortgage to a new lender at renewal without changing the loan balance or the remaining amortization. Same mortgage, new lender. The qualifying rules for straight switches at renewal changed in late 2024. Confirm with your mortgage broker what the current stress test requirements are for your specific situation before comparing rates at other lenders.

Want to Review Your Options Before You Sign?

If your mortgage is renewing in the next 6 to 12 months, do not sign the renewal letter until you understand the full picture: your payment, your equity, your lender options, and whether staying still makes sense for your next five years.

Call Gaurang at 647-892-2411 to talk through the real estate side before you commit to another term.

Gaurang Shah | Shah Team | Royal LePage Flower City Realty

647-892-2411 | mail@myshahteam.com | myshahteam.com

Hindi · Gujarati · Marathi · Punjabi

References

- Bank of Canada, Overnight Rate Target (April 29, 2026): bankofcanada.ca

- Office of the Superintendent of Financial Institutions (OSFI), qualifying rule update for straight switches at renewal (late 2024): OSFI

- WOWA.ca, Mortgage Stress Test calculator (2026):